2025 will undoubtedly be a year of intense tax-related negotiations among lawmakers with the looming expiration of the Tax Cuts and Jobs Act of 2017 and Republicans in narrow control. While it is too early to know concrete tax plans from President Donald Trump’s second term, we have some insight into what he would like to implement as stated on the campaign trail, including:

- Extending most provisions of the Tax Cuts and Jobs Act of 2017, except the State and Local Tax deduction cap may be raised or eliminated.

- Lowering the corporate tax rate to 20% generally and to 15% for domestic manufacturers.

- Exempt from taxes income derived from tips, overtime pay and social security.

How these items will be paid for is largely a guessing game at this point, but municipal market participants worry that possible “pay-for” options may harm the municipal market.

Demand

The common theme of Trump’s wish list is a low tax burden on American taxpayers and companies. All else equal, demand for tax-exempt income diminishes as tax rates fall. Individual tax rates are currently expected to remain at present levels (top rate of 37%), and general corporate tax rates may fall slightly from 21% to 20%.

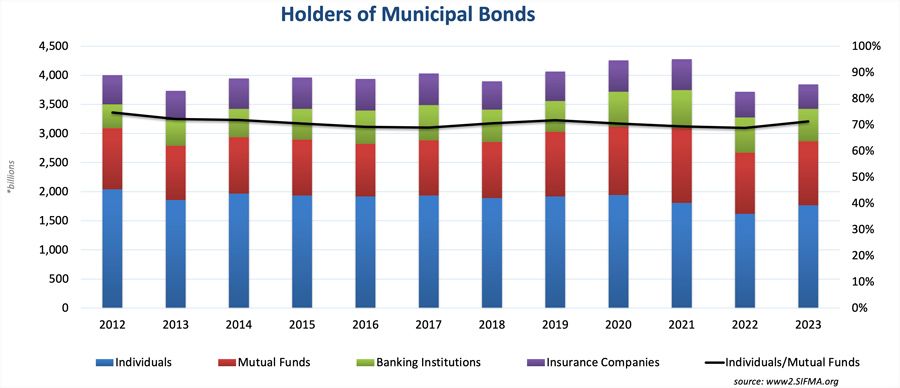

Data from the Securities Industry and Financial Markets Association shows that over 70% of municipal bonds are held by individuals and mutual funds rather than by corporate taxpayers, as shown in the chart below. This was the case even before the Tax Cuts and Jobs Act slashed corporate tax rates.

This means that broad market demand is predominantly driven by individuals rather than corporations. Assuming individual tax rates are not further cut, individuals should still have a strong demand for tax-exempt income. However, entities subject to the corporate tax rate may continue to struggle to find value in tax-exempt municipal bonds.

On the other hand, the State and Local Tax deduction cap has made tax-exempt income more valuable for residents of high-tax states. Trump has expressed interest in raising or eliminating the State and Local Tax cap. There has been support for raising the cap to at least $20,000 for taxpayers who file as married filing jointly. The cap is currently $10,000 regardless of filing status. Any loosening of this restriction may hinder demand for tax-exempt income to some extent but may make it more appetizing for local governments to raise taxes, if needed.

Threatened Tax Exemption

The ability to obtain tax-exempt financing is a tremendous benefit for state and local governments. However, municipal market experts caution that this benefit may be vulnerable due to tax cuts coupled with the recent focus on the national debt. The Tax Foundation reports that if all tax proposals touted on Trump’s campaign trail were enacted, the effect would be a $3 trillion increase in the 10-year budget deficit.1 Eliminating the tax exemption on all municipal bonds could offset about $36 billion per year, according to the Congressional Joint Committee on Taxation. That is a small amount in exchange for being detrimental to the financing of local infrastructure. Therefore, it seems unlikely this will happen.

A more likely scenario is that a segment of the municipal market may lose its eligibility to issue tax-exempt bonds similar to the way advance refunding bonds were obstructed by the Tax Cuts and Jobs Act in 2017. Private Activity Bonds were considered for repeal of the tax exemption when the Tax Cuts and Jobs Act was passed, but ultimately retained their tax exemption for qualified purposes then. Private Activity Bonds are likely to be targeted again. Legislators may look to other segments, such as hospitals or colleges, as additional options to repeal the tax exemption and raise revenue. Borrowing costs would rise for any issuers that lose the ability to issue tax-exempt bonds, which could affect their credit quality. Prohibiting tax-exempt issuance by any municipal subsector would marginally reduce the supply of tax-exempt paper. Also, any changes in tax-free eligibility may lead to a surge in issuance prior to the onset of those adjustments.

As negotiations progress in 2025, it is possible that in the first 100 days of the new administration consequences for the municipal market will be clarified. For now, we expect relatively stable demand for tax-exempt income generally, though banks subject to the corporate tax rate will likely continue to struggle to find value in tax-exempt municipals without seeking long-term bonds. Investors should be watchful for any glimpses of “pay-for” items that could negatively affect issuers or investors.

FOOTNOTES

- “Donald Trump Tax Plan Ideas: Details and Analysis” (Tax Foundation), Oct. 14, 2024. https://bit.ly/4gU9s2O

Dana Sparkman, CFA, Senior Vice President/Municipal Analyst, The Baker Group

Dana is senior vice president, municipal analyst in The Baker Group’s Financial Strategies Group. She manages a municipal credit database that covers more than 150,000 municipal bonds, providing clients with specific credit metrics essential in assessing municipal credit.

The Baker Group is a Preferred Service Provider of the Indiana Bankers Association and an IBA Diamond Associate Member.